Lower Saxony Fiscal Court, 17 August 2010, Ref.: 12 K 10270/09

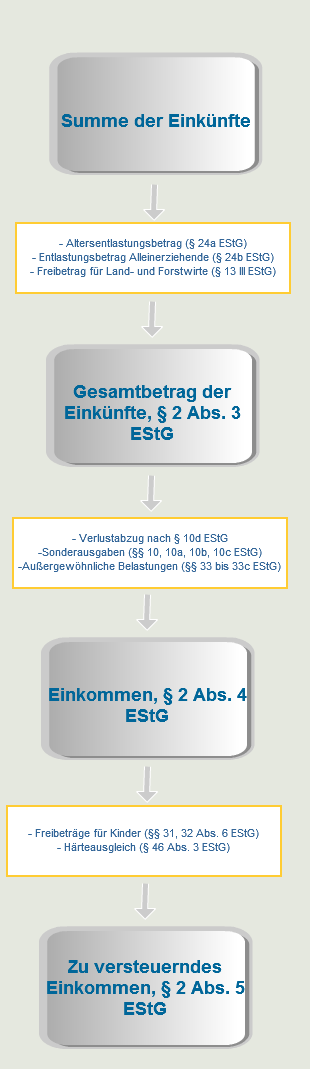

In order to determine the income tax due, the taxable income (Section 2 (5) EStG) must first be calculated, to which the respective tax rate must be applied. This determination is made in four steps:

Adding up the income from the seven types of income (income from agriculture and forestry, from business, from self-employment, from employment, from capital assets, from letting and leasing and other income) results in the total income.

If the respective requirements are met, the old-age relief amount, the relief amount for single parents or the deduction for farmers and foresters can be deducted from this total income, resulting in the total amount of income.

Special expenses and extraordinary expenses can in turn be deducted from this total amount of income to arrive at the income.

If the allowances for children and the hardship allowance are deducted from this income if the requirements are met, the taxable income is finally calculated.

The third step in particular is repeatedly the subject of legal disputes, as taxpayers naturally regard many expenses as deductible special expenses or extraordinary burdens, while the tax office takes the opposite view.

In the above-mentioned judgement, the Lower Saxony Fiscal Court had to decide whether expenses for the removal of dry rot are deductible as extraordinary expenses.

FactsThe plaintiff was the owner of a flat in a residential building from 1900. After real dry rot was discovered in the flat, the expert advised professional dry rot remediation. The remediation of the infested flats in the house cost €128,970.88. The plaintiff's share for the year in dispute was € 10,490.22. In her income tax return for the year in dispute, the plaintiff then claimed € 10,491 as extraordinary expenses. The defendant did not recognise the expenses in the income tax assessment for the year in dispute. After the claimant lodged an objection on the grounds that she would have suffered damage to her health if she had not removed the sponge and this objection was rejected, the claimant sued.

Lower Saxony Fiscal CourtThe Lower Saxony tax court agreed with the plaintiff's view. The plaintiff was entitled to claim the expenses for the removal of the dry rot infestation as extraordinary expenses. The expenses claimed were "extraordinary" within the meaning of Section 33 EStG. Expenses are "extraordinary" within the meaning of § 33 EStG if they are not only unusual in terms of their amount, but also in terms of their nature and reason. The aim of Section 33 EStG is to recognise unavoidable additional expenses for basic living expenses which, due to their exceptional nature, cannot be included in general allowances. Therefore, normal living expenses that are not only incurred by a small minority are not covered by § 33 EStG. Furthermore, only those expenses are covered by Section 33 EStG that are essential and are not covered by either the basic tax-free allowance or the special expenses deduction.

The infestation of a flat with dry rot is a private catastrophe that is more comparable to a house fire or backed-up water than to conventional building defects and is therefore exceptional. According to general perception, this is therefore a special stroke of fate that is not covered by the general way of life.

Source: Lower Saxony Fiscal Court

Important Note: The content of this article has been prepared to the best of our knowledge and belief. However, due to the complexity and constant evolution of the subject matter, we must exclude liability and warranty. Important Notice: The content of this article has been created to the best of our knowledge and understanding. However, due to the complexity and constant changes in the subject matter, we must exclude any liability and warranty.

If you need legal advice, feel free to call us at 0221 – 80187670 or email us at info@mth-partner.de.